- Cryptotwits

- Posts

- The SEC Brought The CFTC To Dinner And They Ordered A 68-Page Joint Rule 📏

The SEC Brought The CFTC To Dinner And They Ordered A 68-Page Joint Rule 📏

Your guide to the big joint SEC/CFTC crypto reveal.

Jonathan Morgan

March 18, 2026

OVERVIEW

The SEC Brought The CFTC To Dinner And They Ordered A 68-Page Joint Rule 📏

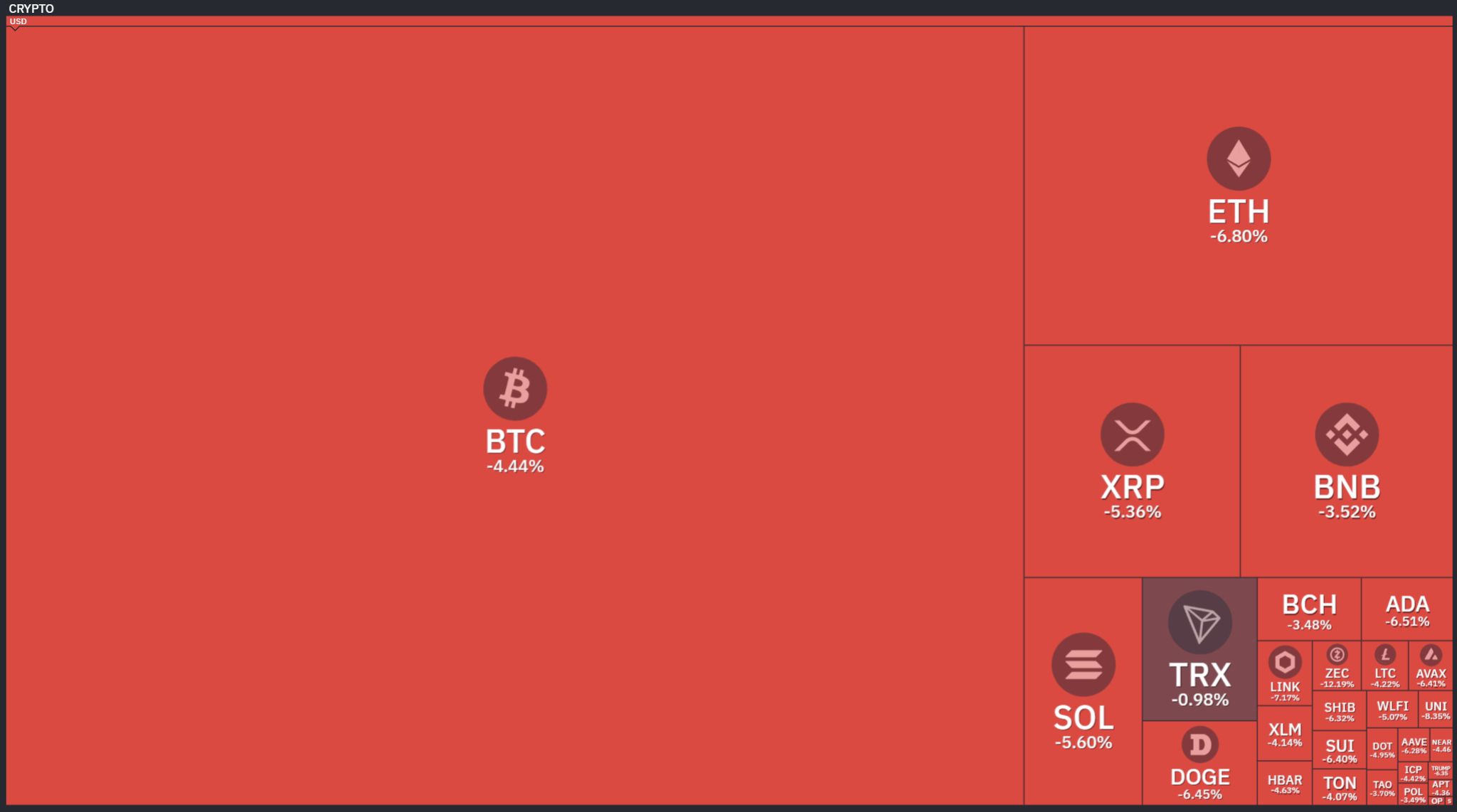

Before we dive in, here’s today’s crypto market heatmap:

Source: finviz

And here’s a look at crypto’s total market and altcoin market cap charts:

Source: TradingView

NEWS

Some Clarity Without CLARITY 😐️

Nine years. That's how long it took. 😱

Nine years since the SEC published The DAO Report in July 2017 and effectively declared war on an industry it didn't understand, using a legal test designed for Florida citrus groves in 1946.

That era ended yesterday.

The SEC and CFTC jointly published Release Nos. 33-11412 and 34-105020: "Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets." It is, by any reasonable measure, the single most consequential regulatory document the crypto industry has ever received from the U.S. government. It is a final rule, an interpretation, and guidance - all wrapped into one 68-page release that does what market participants have been begging for since Coinbase filed its rulemaking petition in 2022: it draws the lines.

Let's break down what this document actually says, what it means for the assets and activities you care about, and who wins and loses from here. Also, I’m not an attorney or a regulator. I’m a stranger. So do your own due diligence on what this stranger is writing.

The Five Categories

This is the real meat of the release. Five categories each with it’s own kind of regulatory weight.

Digital Commodities - assets whose value derives from the programmatic operation of a functional crypto system and from supply/demand, not from someone's managerial efforts. The SEC explicitly names BTC, ETH, SOL, ADA, LINK, XRP, DOT, AVAX, LTC, DOGE, SHIB, APT, BCH, HBAR, XLM, and XTZ. ALGO and LBC make the list too despite lacking CFTC-regulated futures. A digital commodity is not a security.

Digital Collectibles - NFTs, meme coins, fan tokens. CryptoPunks, Chromie Squiggles, WIF, VCOIN all land here. Not securities - value driven by community dynamics, not managerial effort. The Commission even leaves the door open for a meme coin to graduate to digital commodity status if it gains real system functionality.

Digital Tools - functional assets like memberships, credentials, tickets. ENS names, Consensus tickets. Not securities.

Stablecoins - split treatment. Payment stablecoins under the GENIUS Act (enacted July 2025) get a statutory exclusion from the securities definition. "Covered Stablecoins" per the April 2025 staff statement also clear Howey even before the Act kicks in. Yield-bearing or investment-flavored stablecoins? Still potentially securities.

Digital Securities - tokenized stocks, bonds, notes, investment contracts. Putting a security on-chain doesn't change what it is. Bolting on utility features doesn't strip the label either.

Finally. 😅

NEWS

The Investment Contract Framework: Things Don’t Have To Remain A Security Forever 🤯

The SEC pins the Howey analysis to what the issuer actually told buyers - not CryptoBro420 said in a Discord or Telegram channel. 🤣

And the Commission applies three filters to determine whether those representations actually create an investment contract:

Timing - promises must be conveyed before or at the point of sale - post-sale statements don't retroactively create a securities offering.

Channel - official websites, whitepapers, and regulatory filings create reasonable expectations; Discord shitposting generally doesn't.

Specificity - detailed business plans with milestones and funding sources carry weight; vague aspirational language with no actionable substance doesn't.

The "once a security, always a security" thesis is dead. A non-security crypto asset can separate from an investment contract two ways: the issuer fulfills its promises (the clean exit), or the issuer fails and enough time passes that no one can reasonably expect delivery anymore (the ugly exit). 🦢

NEWS

Mining, Staking, Wrapping, & Airdrops ✈️

The release drops explicit safe harbors for four crypto-native activities. Each one removes a regulatory overhang that has been choking infrastructure development for years while the SEC pretended not to notice. 🧑🦯

Mining - solo and pool participation on proof-of-work networks - is not a securities transaction. Miners contribute computational resources, earn protocol rewards. That's administrative work, not passive profit from someone's managerial genius. Pool operators coordinate resources, but last time anyone checked, coordination isn't enterprise management. Took seven years to put that in writing. 🤦

Staking - all four variants (solo, self-custodial with a third party, custodial, and liquid) - gets the same treatment. Staking secures the network, rewards compensate for services rendered. Simple enough that it shouldn't have required a formal release, but here we are.

Wrapping - depositing a crypto asset and receiving a one-for-one redeemable wrapped token - not a securities transaction when the underlying is a non-security. The process is administrative, deposited assets are locked and can't be lent or rehypothecated.

Airdrops of non-security crypto assets where recipients provide no consideration don't create investment contracts - you can't satisfy Howey's "investment of money" prong with something you never gave. The SEC scopes this tightly: task-based airdrops (do X, get tokens) fall outside the safe harbor. But retroactive airdrops to prior users who had no idea they were coming? Clean.

That feels good. 🫂

NEWS

Oh Hai, We’re The CFTC And This Is What We Do 👋

In case you forgot, this is a join SEC/CFTC document. 🫡

The CFTC signed on, confirming it will administer the Commodity Exchange Act consistently with this interpretation. Any non-security crypto asset - other than a payment stablecoin under the GENIUS Act - could qualify as a "commodity" under the CEA.

The SEC handles securities, the CFTC handles commodities, and the two agencies have finally agreed on where the line sits. The turf war that cost the industry half a decade of regulatory paralysis is over. 🥲

NEWS

Winners, Losers, & Operational Implications 🧠

Winners

Every project whose token got named a digital commodity - six of the top ten by market cap - now has definitive confirmation their token is not a security and secondary market trading doesn't trigger securities law.

Exchanges listing those assets no longer face the existential threat of being reclassified as unregistered securities exchanges overnight.

Staking providers, mining pools, liquid staking protocols, and bridge operators all got explicit safe harbors for doing exactly what they've been doing.

Liquid staking protocols can operate without securities registration. Wrapped token providers have a legal framework. Airdrop programs - crypto's primary user acquisition tool - have a clear path to avoid securities treatment if structured right.

Losers

Projects that raised capital with whitepapers full of milestone commitments they never delivered on are still on the hook. The investment contract framework doesn't retroactively forgive vaporware.

Yield-bearing stablecoins and tokens with passive income characteristics remain in securities territory.

Restaking is explicitly excluded - the SEC noted it, declined to address it, and walked away. If you're building there, you're still flying without instruments.

Anyone running a staking service that guarantees fixed reward amounts or exercises discretion over depositor assets is outside the safe harbor. The SEC drew a hard line between ministerial service provision and discretionary asset management. One is covered. The other isn't. 🔃

NEWS

What This Doesn't Do - and What Comes Next 🤔

The SEC is fairly upfront about what this isn't. It doesn't replace Howey - it interprets how Howey applies to crypto. It's the Commission's "first step," open for public comment, subject to revision. 📜

Live, but not set in stone.

What it doesn't touch is a longer list than what it does:

No tailored disclosure frameworks for crypto securities.

No registration pathways for crypto intermediaries.

No mechanics for how digital securities should be offered and traded.

No guidance on DeFi protocols as entities, broker-dealer or exchange registration for decentralized platforms, or cross-border coordination beyond the CFTC partnership.

Those are separate workstreams under Project Crypto and the SEC's Spring 2025 Unified Agenda - which is bureaucrat for "we'll get to it when we get to it."

The Commission also acknowledges the five-category taxonomy isn't exhaustive. Some assets won't fit cleanly. Some will span multiple categories. The framework is a starting point. But a good one. Finally. ☺️

In A Nutshell

It's not perfect, it's not comprehensive - but it's real, it's binding on SEC and CFTC staff, and it draws lines that market participants can actually plan around.

The regulatory overhang that suppressed U.S. crypto capital formation, drove talent offshore, and baked a permanent risk premium into digital assets is being systematically unwound.

Taxonomy established.

Investment contract framework has an exit mechanism.

Mining, staking, wrapping, and airdrops have safe harbors.

The SEC and CFTC are coordinating instead of competing. For the first time in nine years, the rules are written down.

We’ll keep you updated if and when something changes. 👍️

STOCKTWITS

Latest Stocktwits Podcasts & Videos 😱

The Latest Cryptotwits Podcast - Fear & Greed Still in the Fetal Position… But Crypto’s Quietly Bouncing

The Howard Lindzon Show - America vs China: The AI Approval Gap Nobody's Talking About

Boardroom Exclusives - Xanadu CEO Christian Weedbrook on Going Public and the Future of Quantum Computing

True Odds Podcast - March Madness 2026 Predictions: First Round Upsets & Final Four Dark Horses

Philisophical Quant - Fractals Don't Lie (But Headlines Do)

Get In Touch 📬

Email me, Jonathan Morgan, feedback; I’d love to hear from you. 📧

Follow me on Stocktwits 🫂 And Sponsor this newsletter 😎

How Was Cryptotwits Today? |

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital, and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The Content is to be used for informational and entertainment purposes only and the Service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which Content is published on the Service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter holds positions in AVAX, ADA, PUDGY, WLC, IMX, XTZ, NEAR, HBAR, ALGO, INJ, LTC, LINK, ZEC, XLM, and FET. 📋