- Cryptotwits

- Posts

- We've Hit 'Extreme Fear' So Many Times It Should Just Be Called 'Regular Fear' by Now 🤣

We've Hit 'Extreme Fear' So Many Times It Should Just Be Called 'Regular Fear' by Now 🤣

I made myself laugh with that headline.

Jonathan Morgan

March 20, 2026

Sponsored by

OVERVIEW

We've Hit 'Extreme Fear' So Many Times It Should Just Be Called 'Regular Fear' by Now 🤣

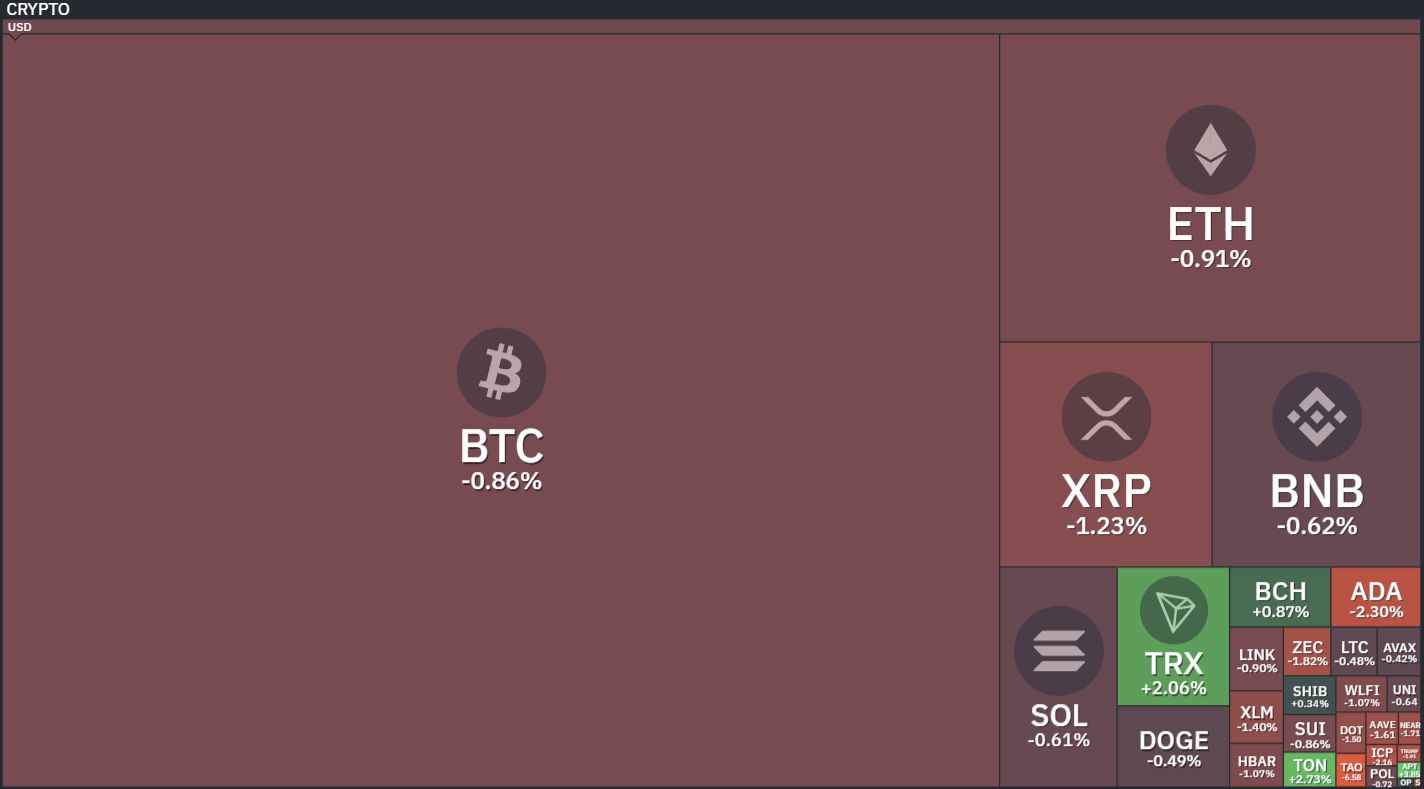

Before we dive in, here’s today’s crypto market heatmap:

Source: finviz

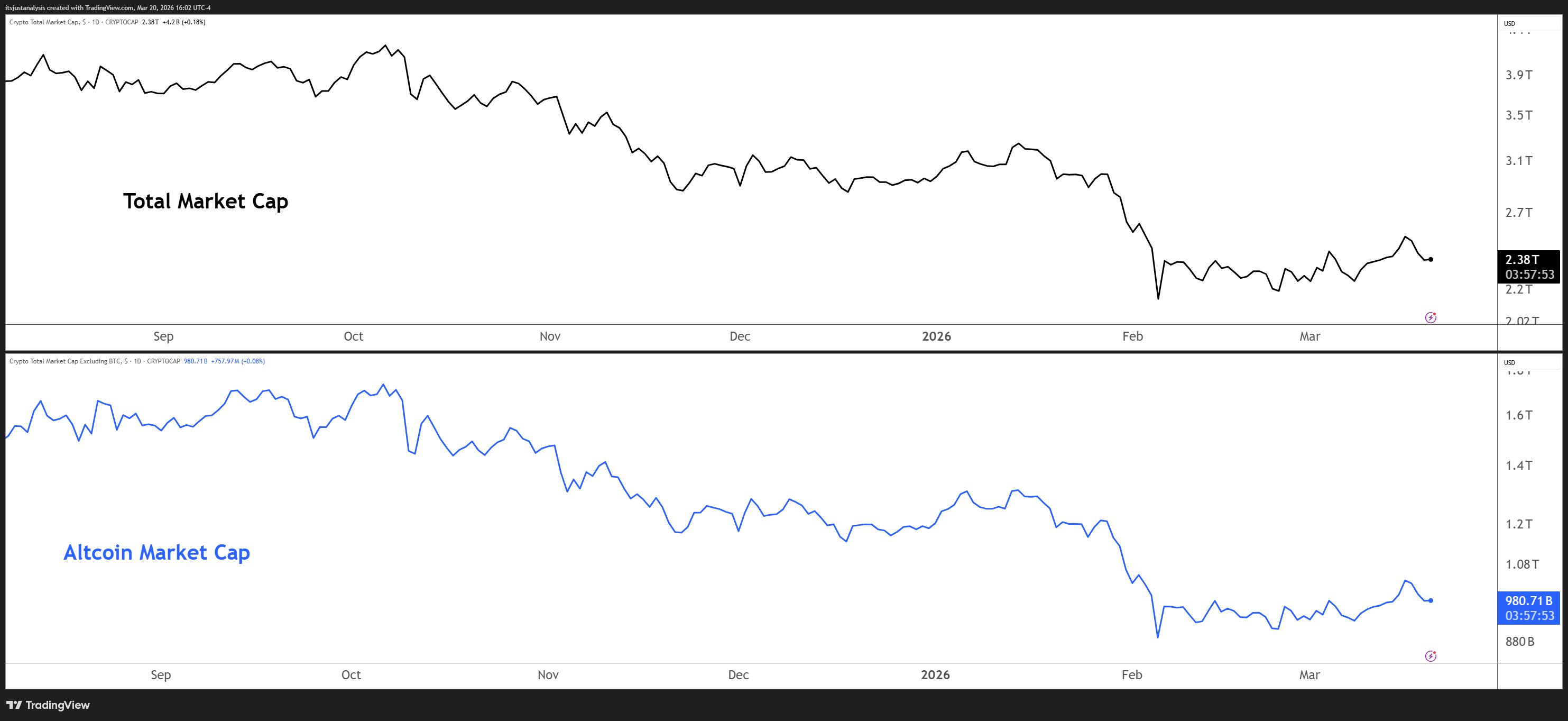

And here’s a look at crypto’s total market and altcoin market cap charts:

Source: TradingView

ON-CHAIN ANALYSIS

On-Chain Is The Way 👍️

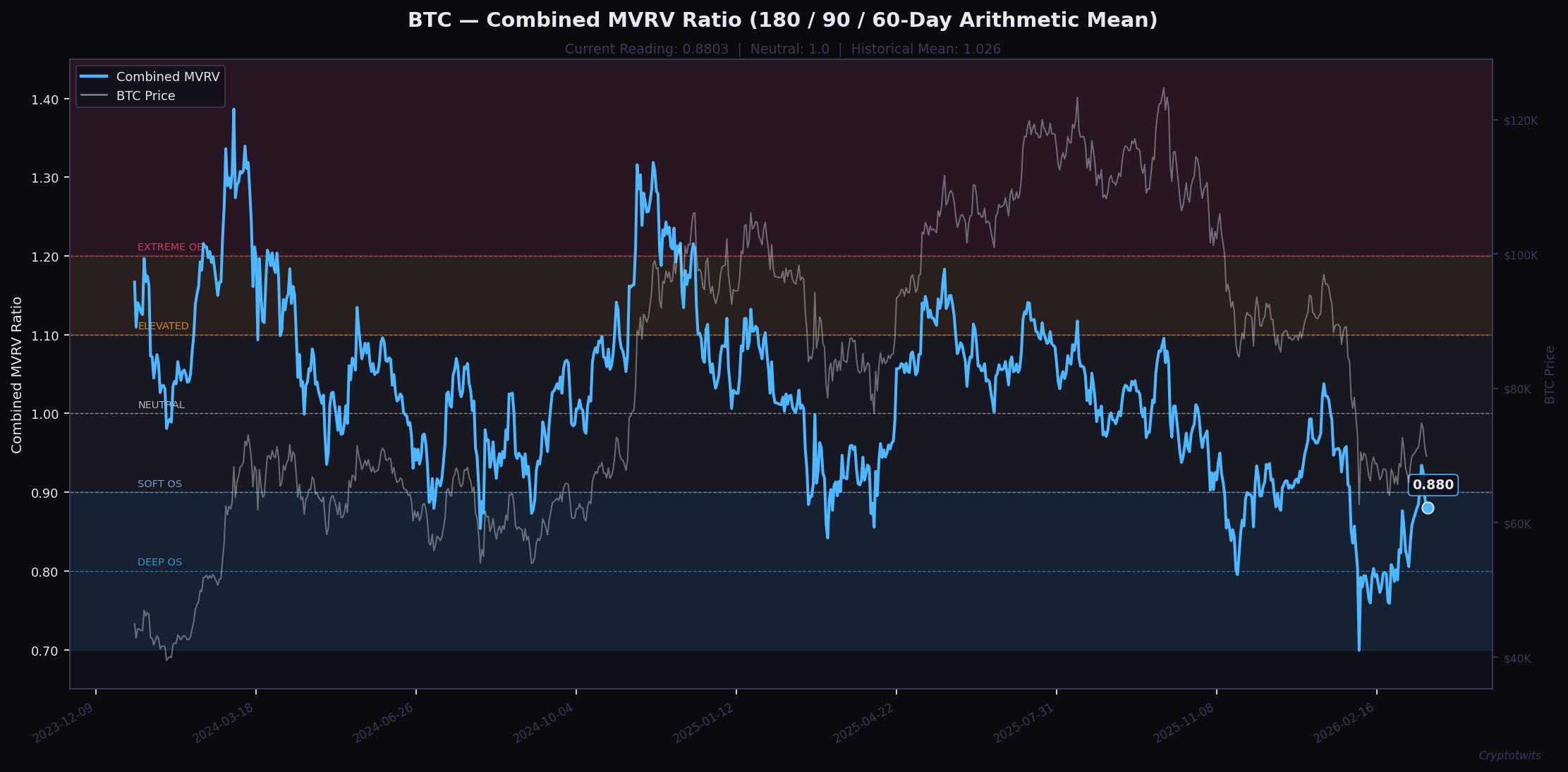

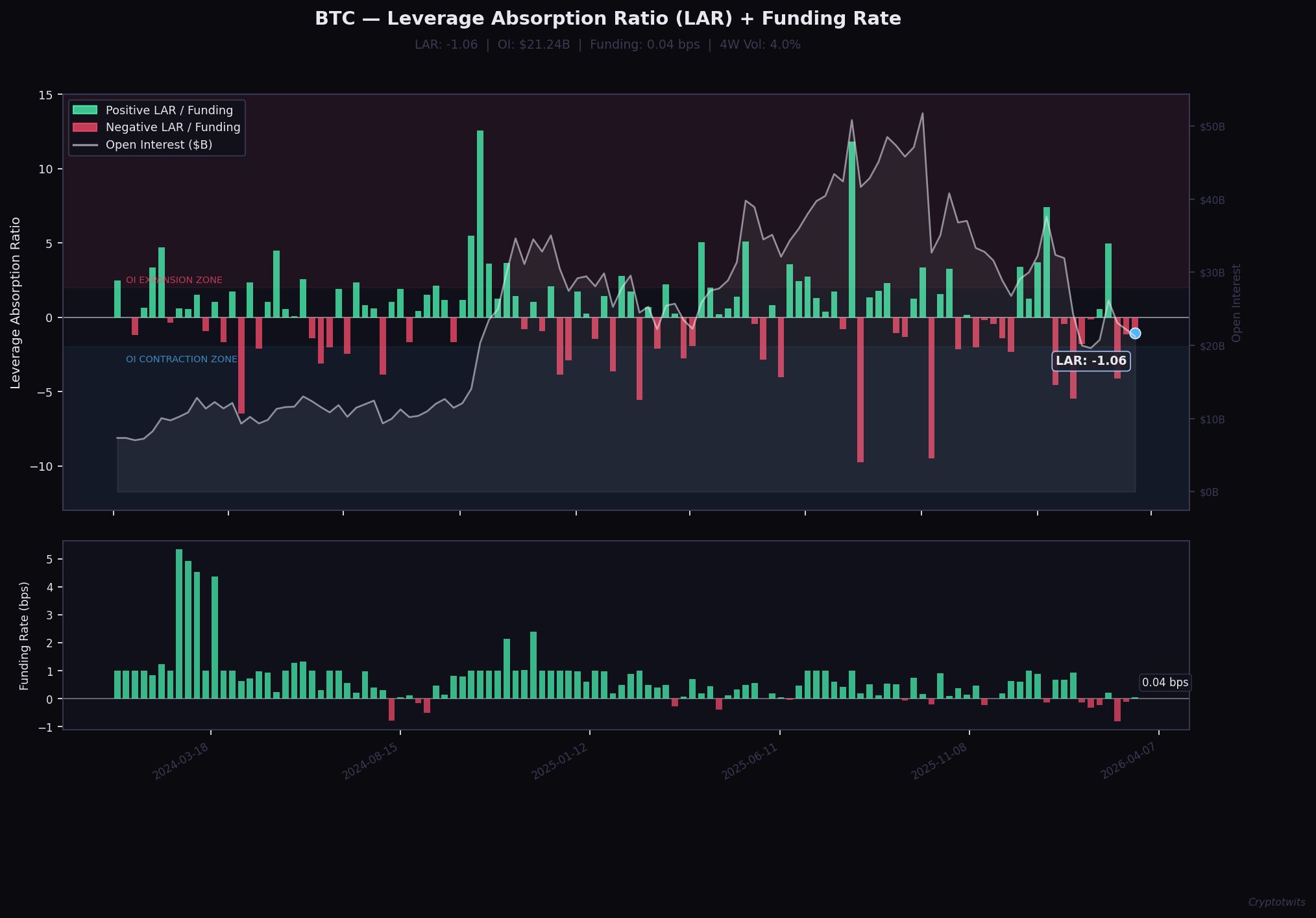

Today's newsletter focuses on how several crypto tickers are doing based on two on-chain analytics measurements. The combined MVRV and the Leverage Absorption Ratio (LAR). 🥈

The combined MVRV is the arithmetic mean of the 60, 90, and 180-day ratios and gives a composite picture of where the average coin sits relative to its cost basis across medium-term windows.

The Leverage Absorption Ratio pairs that with the derivatives side - measuring whether open interest growth is happening in conditions that can structurally support it, using volatility and funding as the weight.

Let's get into it. 👇️

ON-CHAIN ANALYSIS

Bitcoin - Clean Enough to Rally, Cold Enough to Chop 🔪

Combine MVRV - Click to enlarge.

BTC’s combined MVRV is sitting at 0.879 and is currently below the 1.0 line for the fourth consecutive week, meaning the average coin acquired across all three lookback windows is currently held at an unrealized loss relative to its cost basis.

LAR - Click to enlarge.

The LAR reading reinforces that frame without amplifying it. Open interest has contracted from a peak of roughly $37.6 billion in the first week of January to $21.2 billion as of March 19 - a 44% drawdown in notional leverage over ten weeks.

That is a substantial flush.

The LAR has printed negative for three straight weekly periods, with the heaviest deleveraging concentrated in the late-January and early-February window when LAR touched -5.5 and -4.1 respectively. The market is still bleeding leverage, just not hemorrhaging it.

What makes the setup genuinely neutral rather than a clean oversold buy signal is the funding rate - nearly zero at 0.0004 basis points. No conviction from the derivatives side. Volatility has compressed back to the 4% range after spiking above 11% in mid-February.

Near-term lean: neutral-to-slightly-oversold. Structure is tidier than price gives it credit for, but this needs a catalyst. Without OI rebuilding and funding turning positive on upward price action, this market chops and grinds more than it runs. 🥩

SPONSORED

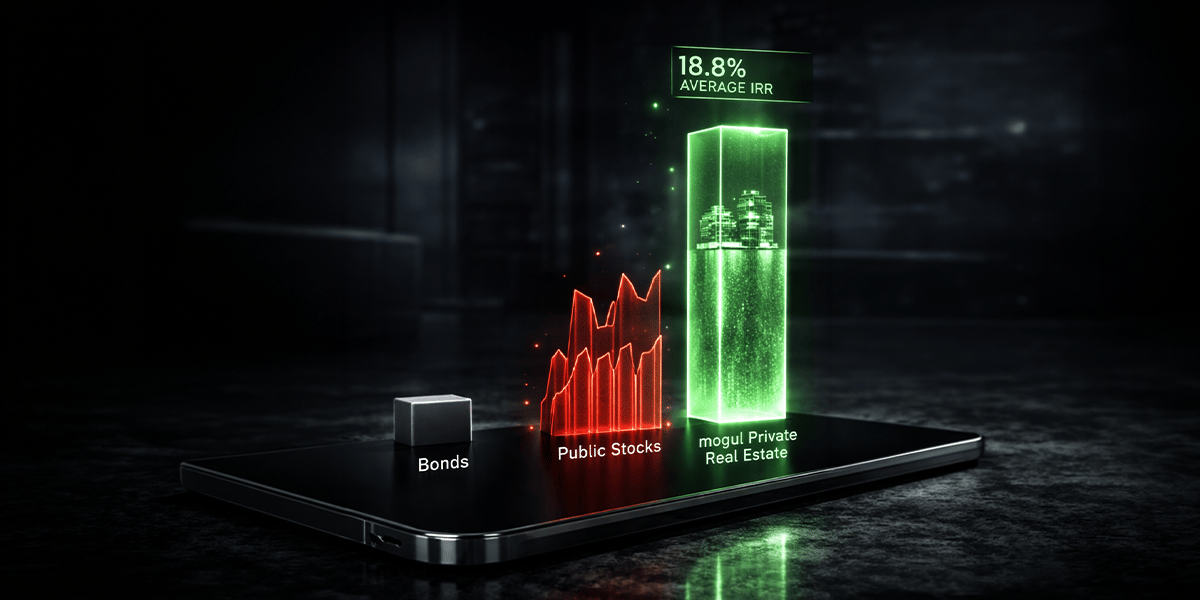

Your $4T Wealth Multiplier: Secure an 18.8% return

Why settle for 2% dividends when Wall Street dominates a $4 trillion market yielding 3x that? You can access the Goldman Strategy thanks to mogul.

They let you invest in elite rentals for less than the cost of a new Rolex. The Ex-Goldman veterans who handled $10 billion of institutional capital even pick the properties and manage them for you. That means all you need to do is watch the rent checks hit your bank account and relax.

Here’s The Breakdown:

7-12% Annual Cash Yields

18.8% Average Annual IRR for superior long-term growth.

Full Tax Benefits of direct real estate ownership.

Stop watching from the sidelines while institutional giants harvest the yield in your neighborhood. Secure your share of the most resilient asset class on earth today.

Past performance isn't predictive; illustrative only. Investing risks principal; no securities offer. See important Disclaimers

ON-CHAIN ANALYSIS

Ethereum - The Leverage Is Gone and the Market Is Paying Shorts to Stick Around 😶

Combined MVRV - Click to enlarge.

Where BTC's MVRV distribution skews modestly above 1.0 since 2024, ETH's mean sits almost exactly at neutra. The cycle floor on this metric came in at 0.602, so there's still room lower, but at 0.828 you're already deep in the zone where coins are underwater against medium-term cost basis across all three windows simultaneously. ⭕️

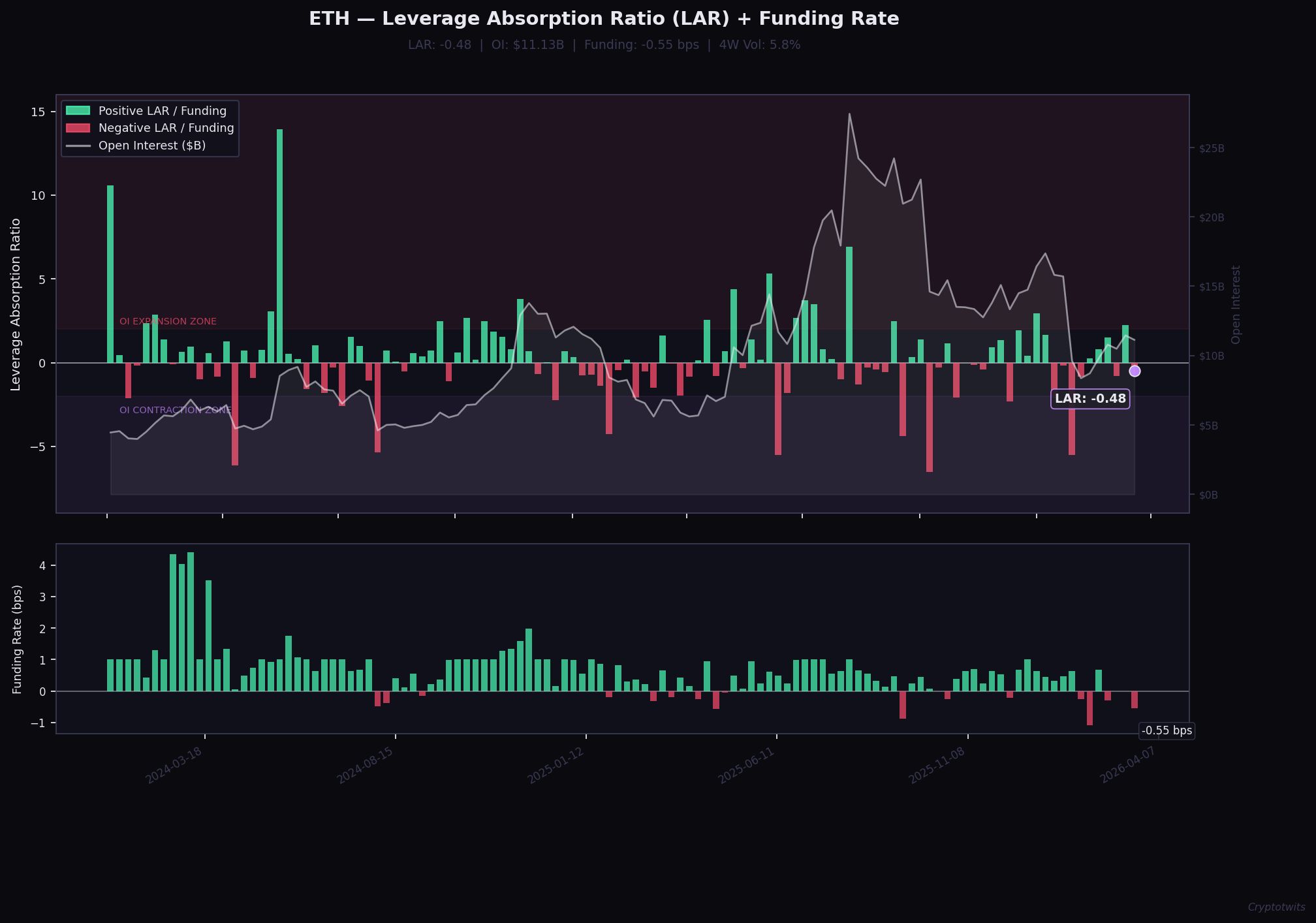

LAR - Click to enlarge.

What separates ETH's setup from BTC's is the magnitude of the leverage flush. Ethereum OI collapsed from a local high near $18B in early January to $11.1B as of March 19 - a roughly 38% drawdown in notional positioning.

The LAR registered its most violent contraction in the late-January window at -5.53, triggered by the same macro shock that clipped BTC's OI. Since then, ETH's LAR has oscillated without building durable positive momentum.

Also: ETH funding is running negative - meaning the marginal derivatives participant is leaning short or hedged, not long. Combined with 5.8% four-week volatility still elevated from the February washout, it looks like a cold market with residual uncertainty baked into the cost of carry.

Near-term lean: oversold with no catalyst in sight. The structural cleanup is there - OI is lean, positioning is not crowded long - but negative funding and a stalled MVRV recovery say demand hasn't shown up to take the other side. ⚖️

ON-CHAIN ANALYSIS

Chainlink - Below Cost Basis, Below Its Own Mean, and Shorts Are Getting Paid 🤑

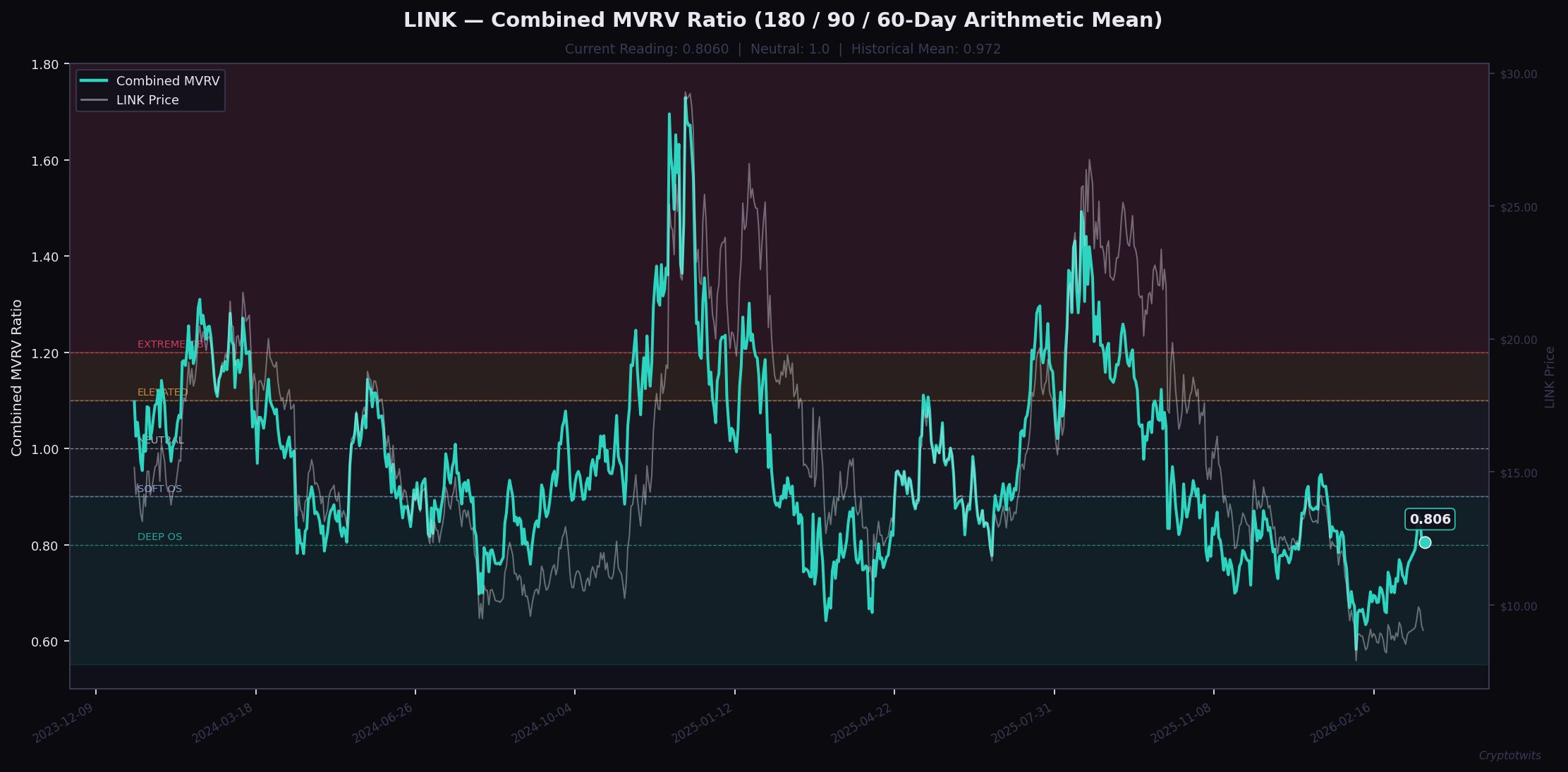

Combined MVRV - Click to enlarge.

Chainlink's average cost basis environment since 2024 is structurally more compressed than Bitcoin's or Ethereum's, so reading 0.806 against its own historical norm (well, since 2024 at least) is a worse signal than the raw number implies when viewed in isolation. 😱

Holders across all three lookback windows are underwater, and the gap between current price and break-even cost basis is widening, not closing.

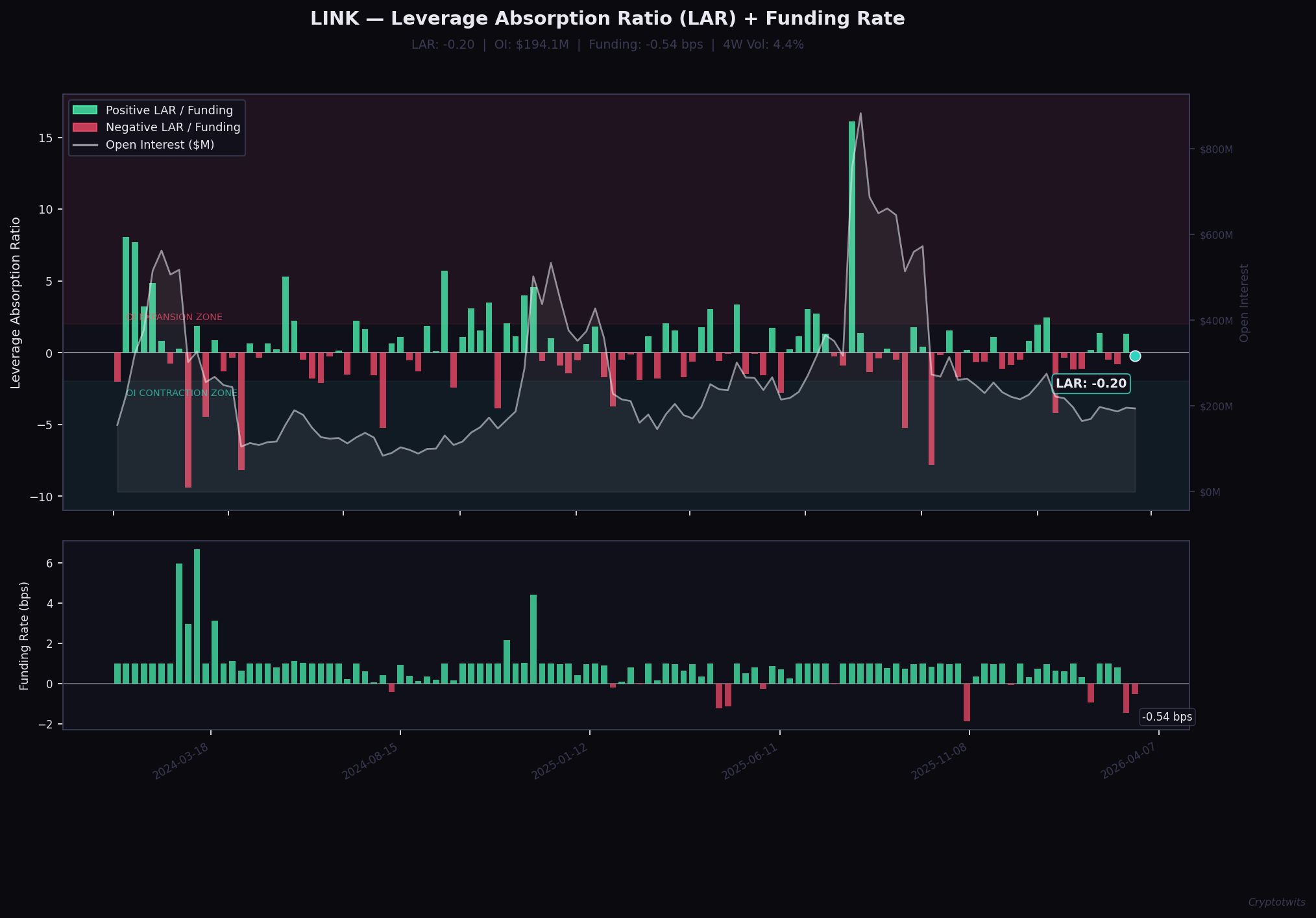

LAR - Click to enlarge.

Total open interest in LINK is thin - $194 million as of March 19, an order of magnitude smaller than ETH's $11B and a fraction of BTC's $21B. Thin OI markets amplify LAR swings in both directions without necessarily reflecting genuine structural change.

What I can say is that the most recent reading comes in at -0.20 - mild negative, suggesting residual OI bleed rather than active forced deleveraging. The violent moves were back in late January and early February, where LINK's LAR touched -9.4, were the worst.

What's left after it is not encouraging. Funding has flipped negative at -0.54 basis points, four-week volatility is running at 4.4%, and OI has not rebuilt in any meaningful way since the January washout. The derivatives market is not pricing in a recovery - it's paying shorts a small premium to stay positioned against it.

Near-term lean: oversold. ⤵️

TECHNICAL ANALYSIS

XRP - The Highest Reversion Potential of the Four & The Least Evidence It’s About To Happen 🧠

Combined MVRV - Click to enlarge.

There’s a fairly good sized gap relative to XRP's own mean (since 2024) of 1.052. Of the four assets here, XRP carries the highest historical mean. 🤷

Reading 0.849 against a mean of 1.052 means XRP is currently running about 20 points below where it tends to equilibrate (is that even a word?) - a wider deviation from its own baseline than either ETH or LINK on the same measure.

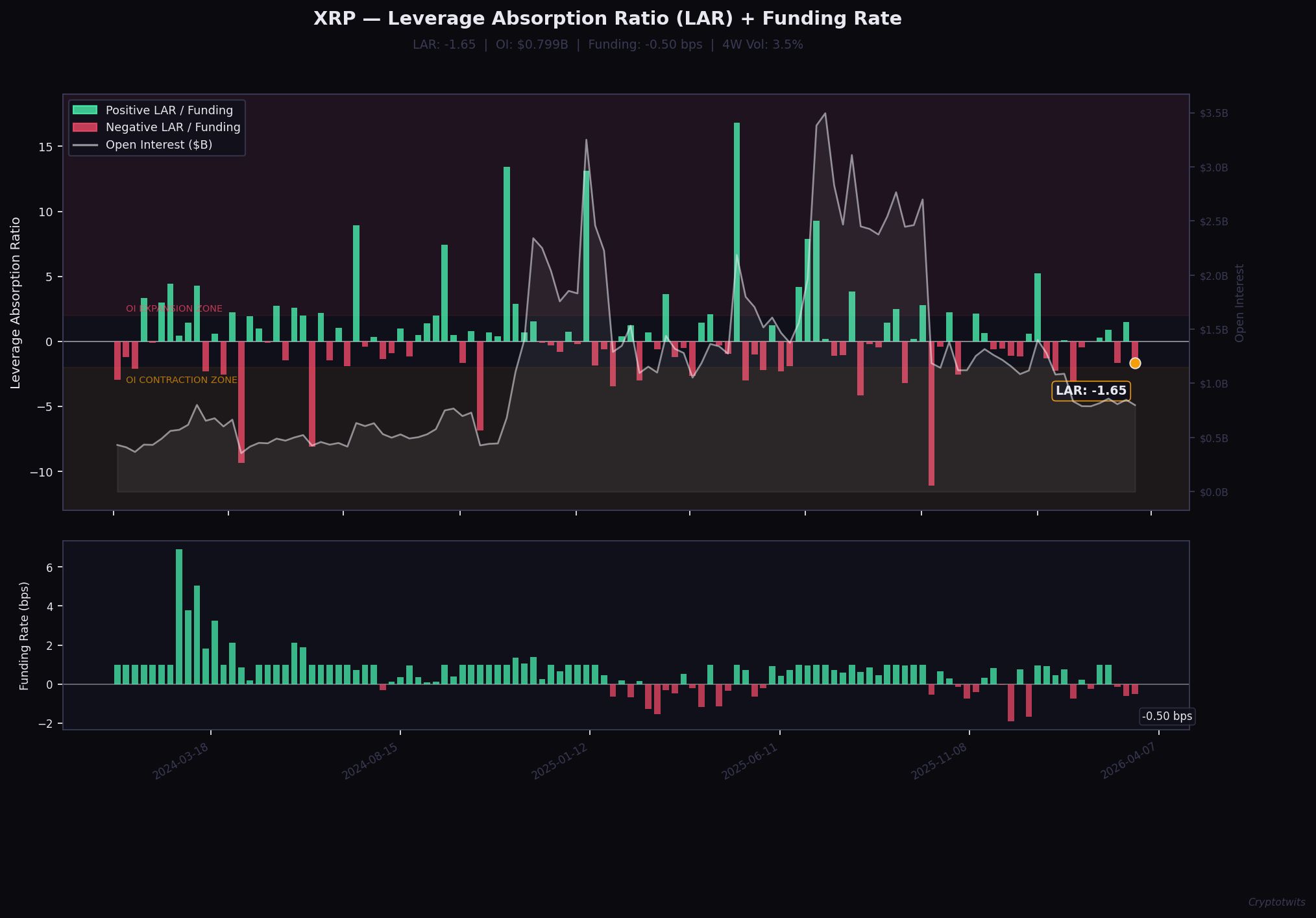

LAR - Click to enlarge.

XRP's LAR has oscillated between mild expansion and contraction since the February floor without establishing any directional conviction. The late-January flush was severe at -3.13, but it wasn't the worst reading in this dataset, and the structural cleanup since then has been partial at best.

Open interest sits at $799 million - down meaningfully from the January highs but not gutted the way LINK's $194 million position looks.

Funding has flipped negative at -0.50 basis points, mirroring ETH and LINK almost exactly. Four-week volatility is the lowest of the group at 3.5%, which sounds constructive until you realize compressed volatility with negative funding and a stalling MVRV is just a market deciding nothing.

Near-term lean: oversold but range-bound. XRP has the highest mean-reversion potential of the group given its historical MVRV range, but that potential has been sitting there unrealized for two months. 📆

NEWS IN THREE SENTENCES

AI, Stablecoins, & Privacy News 🕵️

📱 ZetaChain Built AI Agents With Real Phone Numbers So You Can Text Them Without Downloading Anything

Anuma launched two AI agent phone numbers via ZetaChain's infrastructure, both running on encrypted persistent memory that survives across sessions and model switches, accessible by SMS or iMessage with no app, no login, and no seed phrase. ZetaChain manages the cryptographic identity layer, memory is encrypted client-side and persists across every text conversation, and the AI Portal handles multi-model routing so users can switch between GPT, Claude, and Gemini mid-conversation without losing context. At $5.99/month it's also cheaper than every competitor in the AI texting space. ZetaChain.

⏱️ Curve Fixed the Part Where Moving crvUSD Off an L2 Took Longer Than Filing a Tax Extension

FastBridge cuts crvUSD's seven-day L2 withdrawal window to roughly 15 minutes - a LayerZero message confirms a bridge transaction is in flight, an Ethereum-side vault releases pre-minted crvUSD immediately, and the canonical bridge settles in the background a week later like it was always going to. The real beneficiary is arbitrageurs who can now correct crvUSD price dislocations between L2s and mainnet before the opportunity closes. Curve Finance.

NEWS IN THREE SENTENCES

Real World Asset Tokenization (RWA) News 🪙

🔗 LayerZero and Centrifuge Are Teaming Up So Tokenized Funds Don't Have to Pick a Single Chain and Pray

Centrifuge handles the institutional plumbing for tokenized financial products - structure, controls, compliance - and LayerZero handles distribution across 165+ blockchains without fragmenting liquidity into disconnected versions of the same asset. The first products crossing over include JTRSY, JAAA, and SPXA, expanding across Ethereum, Solana, Avalanche, Base, BNB Chain, and HyperEVM from launch. Centrifuge.

💰 EtherFi Is Routing $6B in Deposits Toward Real-World Yield

EtherFi is integrating Plume's Nest Vault infrastructure to give users access to Superstate's USCC fund through its existing interface without users touching anything offchain. DeFi yields are compressed and increasingly inaccessible to non-technical users; RWA yield through an embedded vault is the cleaner answer for a neobank trying to compete with actual banks on return. The rollout starts with a portfolio reallocation, then moves into the EtherFi interface directly. Plume Network.

NEWS IN THREE SENTENCES

DeFi, DEX, & Lending News 🏦

💳 Uniswap Is Live on Tempo

Tempo is a payments-first chain built for stablecoins with Uniswap v2, v3, and v4 serving as the liquidity layer for everything that isn't a stable-to-stable swap. Any liquidity source on any chain can theoretically plug into Uniswap's routing. The pay-with-any-token skill for Tempo's Machine Payments Protocol lets AI agents swap into whatever token a payment challenge requires and retry automatically. Uniswap.

💵 Yearn Finally Shipped the Cross-Chain Yield Vault

yvUSD is a delta-neutral stablecoin vault built on Yearn V3 that plugs into principal tokens, leverage loops, and RWAs across mainnet and L2s. The optional lock mechanic lets users commit to a 14-day cooldown period for boosted yield, which lets the vault match duration to actual depositor behavior rather than keeping everything in liquid strategies to accommodate unexpected exits. yearn.finance.

🏦 SODAX Stake Is Live and ICX Holders Have Until April 8 to Get Positioned Before Rewards Start

SODAX Stake converts SODA into xSODA. The unstaking options are honest about the tradeoffs: wait the full 6-month period for full value, exit early with up to a 50% penalty, or trade xSODA on the market at whatever the current rate is. ICX migration is fully live now with Stake joining Swap and Migrate - the deadline that matters is April 8, when rewards begin. Sodax.

STOCKTWITS

Latest Stocktwits Podcasts & Videos 😱

The Latest Cryptotwits Podcast - HashPack on Hedera: Kraken Listing, Cross-Chain Swaps, and What’s Next (HashPack Card)

The Howard Lindzon Show - America vs China: The AI Approval Gap Nobody's Talking About

Boardroom Exclusives - Xanadu CEO Christian Weedbrook on Going Public and the Future of Quantum Computing

True Odds Podcast - March Madness 2026 Predictions: First Round Upsets & Final Four Dark Horses

Philisophical Quant - Fractals Don't Lie (But Headlines Do)

Get In Touch 📬

Email me, Jonathan Morgan, feedback; I’d love to hear from you. 📧

Follow me on Stocktwits 🫂 And Sponsor this newsletter 😎

How Was Cryptotwits Today? |

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital, and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The Content is to be used for informational and entertainment purposes only and the Service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which Content is published on the Service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter holds positions in AVAX, ADA, PUDGY, WLC, IMX, XTZ, NEAR, HBAR, ALGO, INJ, LTC, LINK, ZEC, XLM, and FET. 📋